The Everything Bubble

By Christian Schmid on November 22nd, 2022

“Every serious [episode of] deflation I’ve looked at is preceded by an asset bubble, and then it bursts”

Stanley Druckenmiller, hedge fund manager and philanthropist

The phrase “this time it’s different” has been described by the legendary British investor Sir John Templeton as constituting “the four most expensive words in the world”. Templeton was implying that we have seen everything before, and repeat signals that have historically portended a financial tsunami should not be explained away by attempting to justify why it should be different this time around.

However, with the price of the traditional asset classes of stocks and bonds deflating in tandem against a backdrop of inflation at 40-year highs (in the West) and central banks aggressively tightening into a recession, it seems that the bursting of ‘the everything bubble’ is occurring in the exact opposite scenario to that described by Stanley Druckenmiller in the quote above. So, why is it different this time?

Today, it is readily understood that “the everything bubble” refers to a range of investments, including stocks, bonds, and real estate, that, since the financial crisis, have surged in value as central banks left interest rates at rock-bottom levels for years and massively bloated their balance sheets through asset purchase programs funded by electronic money creation.

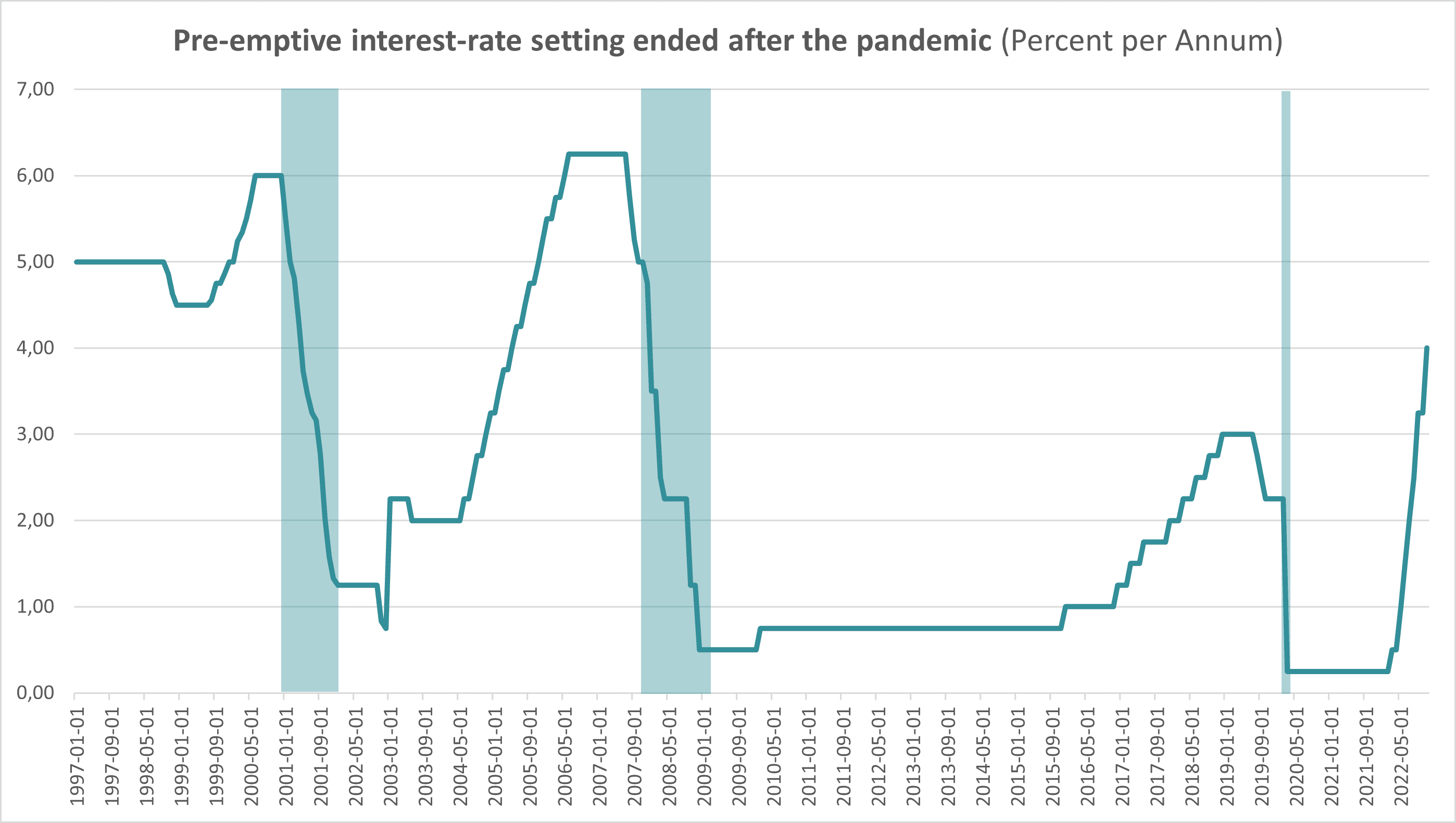

The central banks’ penchant for being ‘accommodative first’ was amply illustrated by the largesse in the reaction to the Covid pandemic, with excessive liquidity being provided long after the economic rebound had begun in earnest. This marked the final nail in the coffin for Alan Greenspan’s vision of pre-emptive, rather than reactionary, monetary policy that had, for the large part, governed US interest rate decisions since the late 1980s.

“The endgame for central bank policy”?

The term “the everything bubble” was first coined by renowned investment analyst Graham Summers, and it formed part of the title of his prescient 2017 book “The Everything Bubble: The Endgame for Central Bank Policy”. This was based on a decade of research, with the author concluding that the final speculative frenzy induced by Federal Reserve overreach represents the proverbial end game for central banks, as their credibility is ultimately shredded.

The following chart illustrates how the Fed was largely able to fulfil this mandate over the course of three decades, and how policy has erred in the years following the Global Financial Crisis (GFC).

As we can see, central banks have typically raised interest rates during economic rebounds to both extend the duration of the recovery phase and to provide the scope to cut rates when the economy tips over into recession. However, following the GFC, the Fed maintained unprecedentedly low interest rates for an extended period. This new paradigm artificially raised risk appetite, causing the everything bubble to inflate rapidly – and what goes up …

Source: International Monetary Fund and St. Louis Federal Reserve (November 2022). Shaded areas denote recessionary periods

Effective diversification has never been such a challenge…

Earlier this year, as the everything bubble began to deflate, Goldman Sachs announced the ‘death’ of the 60:40 (equity/bond) portfolio – a traditional asset allocation model that pension investors have largely adhered to for decades. The irony of the timing of the Goldman Sachs assertion is that ‘60:40’ effectively ‘died’ years ago when the everything bubble was inflating, as neither asset provided any diversification benefit for the other. However, nobody is concerned by a lack of diversification when asset prices are rising in tandem. The everything bubble may not have burst entirely, but it has deflated like yesterday’s party balloon during 2022. So, the big question is how investors can achieve true diversification and insulate their portfolios from the widespread decline in the value of traditional asset classes.

Conventional wisdom would suggest that the most appropriate course of action would be to include an allocation to tangible (or ‘real’) assets, such as gold and other commodities. The issue is that these are priced in US dollars, and the greenback, by virtue of its status as the world’s reserve currency and a safe haven in times of turmoil, has strengthened precipitously.

Dollar strength has been exacerbated by the Fed’s desperate efforts to compensate for its earlier policy error through aggressive tightening and its pledge to defeat spiraling inflation, regardless of the economic cost. As such, commodities as an asset class, as well as other dollar-based assets, are prohibitively expensive for non-US investors.

Private markets: enhanced resilience during downturns…

The investment environment in recent months has been characterized by acute volatility in public markets. Perceptive investors are increasingly appreciating the potential of gaining exposure to private-market, growth equity, where a long-term focus on value creation predominates. In short, capital committed to private market investments, such as growth equity, venture capital, and private equity, is referred to as ‘sticky money’ because typical investors are committed to investing over the medium term, over which they can harvest the progressive value creation of pre-IPO companies operating in niche markets or those with an organic competitive edge.

Given perceived or actual barriers to entry, these investment opportunities are typically far less liquid than positions in public equity and bond markets. As such, positions are not overcrowded, and we are highly unlikely to witness a ‘rush for the exits’ typically associated with a bubble bursting. Similarly, the opportunity for ‘buy-the-dip’ investors is severely constrained because valuations are primarily based on fundamentals rather than supply and demand. Secondary-market entry points are also subject to a much more limited supply. These factors collectively lead to a much lower level of volatility in private markets, relative to their public market counterparts.

Although yields in the traditional bond markets have increased dramatically this year, this has come at some cost to existing holders, while defining an attractive entry point remains a difficult task. As explained above, we should typically see higher interest rates, lower inflation, and more attractive ‘real yields’ at this stage of the economic cycle. Moreover, the trajectory of central bank policy remains the subject of almost daily speculation.

Growth investing – from FAANGtastic to pragmatic

Following a decade in which positions in the FAANG (Facebook – now Meta Platforms, Amazon, Apple, Netflix, and Google – now Alphabet) stocks became increasingly overcrowded, the calendar year of 2022 has seen this component of the everything bubble burst in dramatic style. However, this is simply a case of massively overvalued stocks being brought down to earth with a bump. It certainly does not signal a ‘growth hiatus’.

All the ingredients for a continued advance in growth-related investments remain firmly intact. These include macro tailwinds and the ongoing megatrends in certain industries, such as the digitalization of healthcare. However, we believe a pragmatic approach, from the perspective of analyzing the market in a way that adjusts in accordance with prevailing conditions, is more objective than simply buying into the broad growth concept.

In our view, the uncertain trajectory of central bank policy means that it is important to steer clear of leverage as far as possible in order to reduce interest-rate sensitivity. But the positive impact of the prevailing environment is that we are able to secure deals at cheaper valuations. In contrast, we have yet to see a similar cheapening in the leveraged buy out (LBO) market, which reinforces our conviction in the value of the growth equity proposition – particularly where the investment bias is towards sectors that continue to see healthy growth.

Bringing it all together…

For investors to take full advantage of the diversification opportunities presented by private-market investments, it is important to appreciate that some perceived barriers to entry are just misperceptions.

For example, some of the perceived barriers to entry are:

Private markets are only accessible to the most sophisticated investor classes

Investors have to put ‘all their eggs in one basket’ because of limited deal participation

There are no indexing opportunities for non-sophisticated investors

It is not possible to build a self-select portfolio

There is no secondary market, so investors are unable to exit early if they wish to

Private markets are, in fact, widely accessible. However, it is often the case that outstanding deals are oversubscribed quickly. The ability to participate can also depend on existing relationships with General Partners (GPs), making access prohibitive for new entrants and/or potential participants wishing to make a small initial allocation. So, there is some substance to this misperception, but the remaining four listed above are simply false.

In the era of ‘the everything bubble’, we find that increasing numbers of visionary investors are turning to private markets to enhance their diversification potential. Is it time you considered an allocation to growth equity?

Introducing the Stableton Unicorn Index AMC

Learn how an allocation to the most exciting and rapidly growing privately held companies can help to boost your portfolio.