Time to Invest in Growth Equity?

By Christian Schmid on October 22nd, 2022

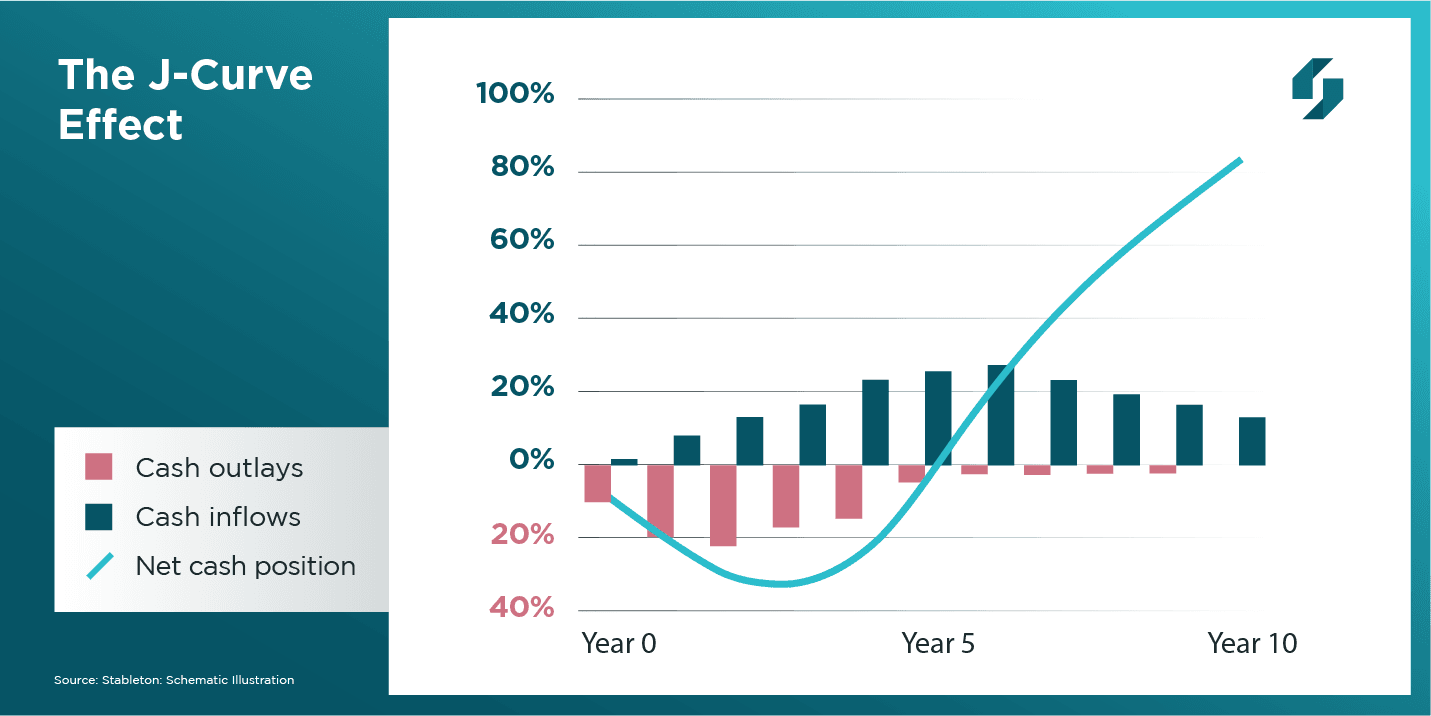

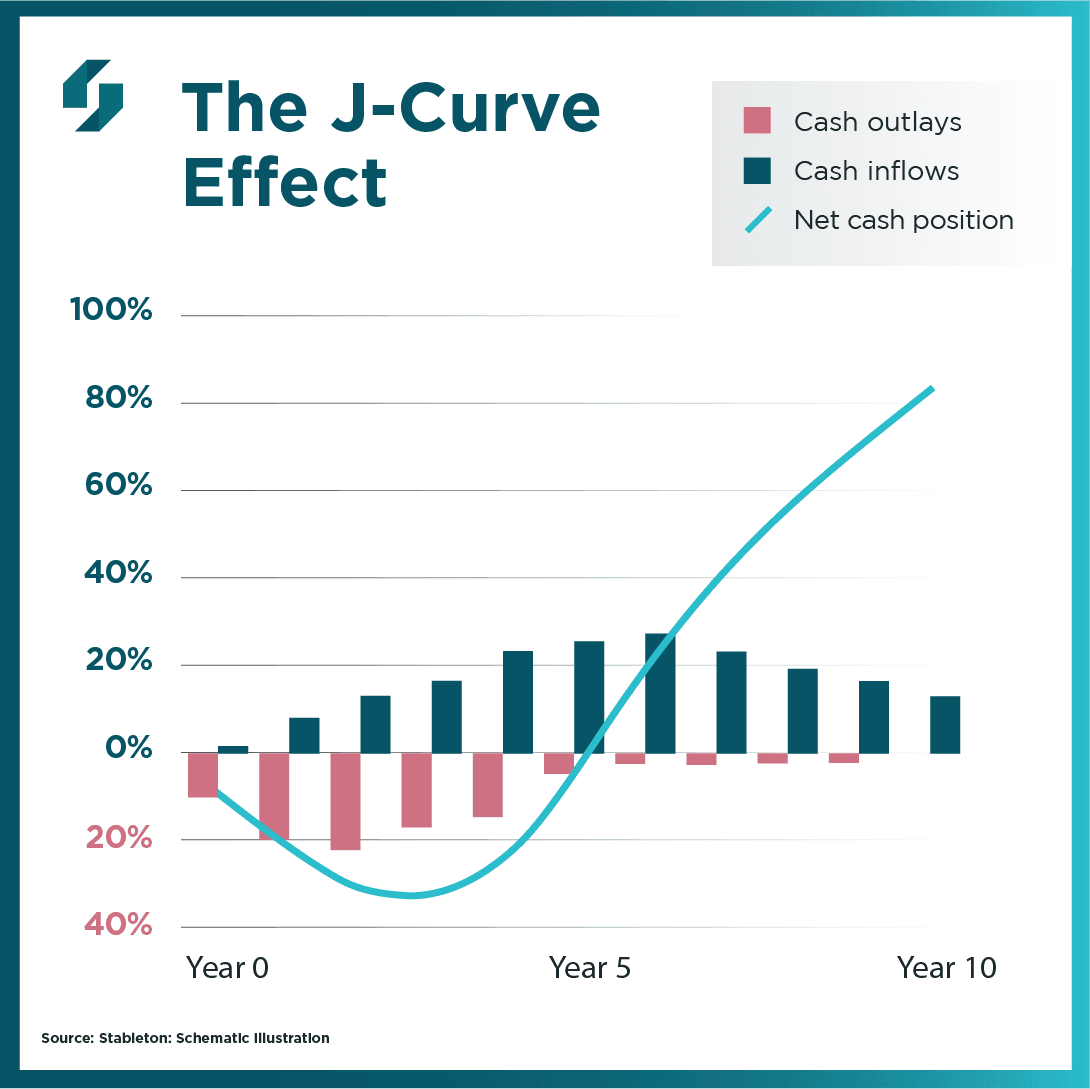

The prevailing investment environment is characterized by acute volatility in public markets. At every inflection point, the number of investors seeking to buy the dips appears to recede, resulting in a gradual, albeit bumpy, grind lower and continually deteriorating investor sentiment. Fortunately, there is an alternative, and perceptive investors are increasingly appreciating the potential of gaining exposure to private-market, growth equity, where a long-term focus on value creation predominates. This is an important consideration as investors have made a conscious commitment to the project they are backing. This means that knee-jerk selling is unusual, and there is an absence of ‘market timers’ because value creation is progressive. The latter aspect is perfectly illustrated by the J curve. In private equity, the J Curve represents the tendency of companies to post negative returns in the initial years, due to capital expenditure and lack of revenues, and then realize rising gains in later years, when cash inflows increasingly exceed outlays. A simple rule of thumb is the steeper the J curve, the more lucrative the investment.

More than a portfolio diversifier…

Although private equity is often touted as a good portfolio diversifier because of its low overall correlation to traditional stock market investments, it is often overlooked that this lack of correlation can be partly attributed to the historical ability of the asset class to deliver robust returns in times when conventional growth becomes increasingly elusive. For many, this concept is counter-intuitive because private equity is generally classified as a high-risk, high-return asset class. Surely, these risks are intensified in hostile trading conditions? In fact, analysis of returns in the first two decades of the new millennium paints a completely different picture. During this period, growth equity only underperformed stock markets in ‘bull’ years (when major equity indices registered double-digit gains)1. Interestingly, growth equity recorded its strongest relative outperformance in 2008, the year in which the global financial crisis reached its peak, and stock markets registered their most negative return1. Given those return dynamics, it is unsurprising that some attributes of private equity provide a distinct advantage in difficult market conditions. In the opening paragraph, we alluded to the ‘stickiness’ of capital by virtue of the patient and committed nature of the typical investor. A further point to consider is that, during downturns, deals are often renegotiated on more investor-friendly terms, as infant companies find capital even more difficult to come by from other sources during times of low liquidity. Consequently, some of the strongest returns recorded in growth equity have stemmed from deals secured in years of substantial economic malaise, such as 2001, 2002, and 2009.

Better than a ‘port in a storm’…

With many leading indicators implying that the risk of global recession is increasing as each month passes, it is an opportune time for investors to consider whether private markets could potentially provide a ‘port in a storm’. However, as we have seen, historical performance trends suggest that there is far more substance to the private-market, growth equity opportunity than mere capital preservation. Deals to harness medium-term value creation can be secured at substantial discounts during economic downturns. At the same time, participating investors are much less likely to head for the exits at the first hint of difficulty. These two attributes (increased growth potential and lower volatility) are the essential ingredients of superior risk-adjusted returns.

Introducing the Stableton Unicorn Index AMC

Learn how an allocation to the most exciting and rapidly growing privately held companies can help to boost your portfolio.