The Future of Banking: For Revolut, the Term “Neobank” Is Something of an Understatement

The app that solved a problem

Revolut founder and CEO Nikolay Storonsky had been a derivatives trader at Credit Suisse, working with his friend and software engineer Vladyslav Yatsenko, when they decided to move to a London fintech incubator. Having traveled extensively, Storonsky was irritated by expensive foreign exchange fees, so together, the pair developed an app to save travelers paying these excessive charges. Creating an inexpensive digital solution to fix a historic consumer problem is by now a fintech trademark.

Why is Revolut different?

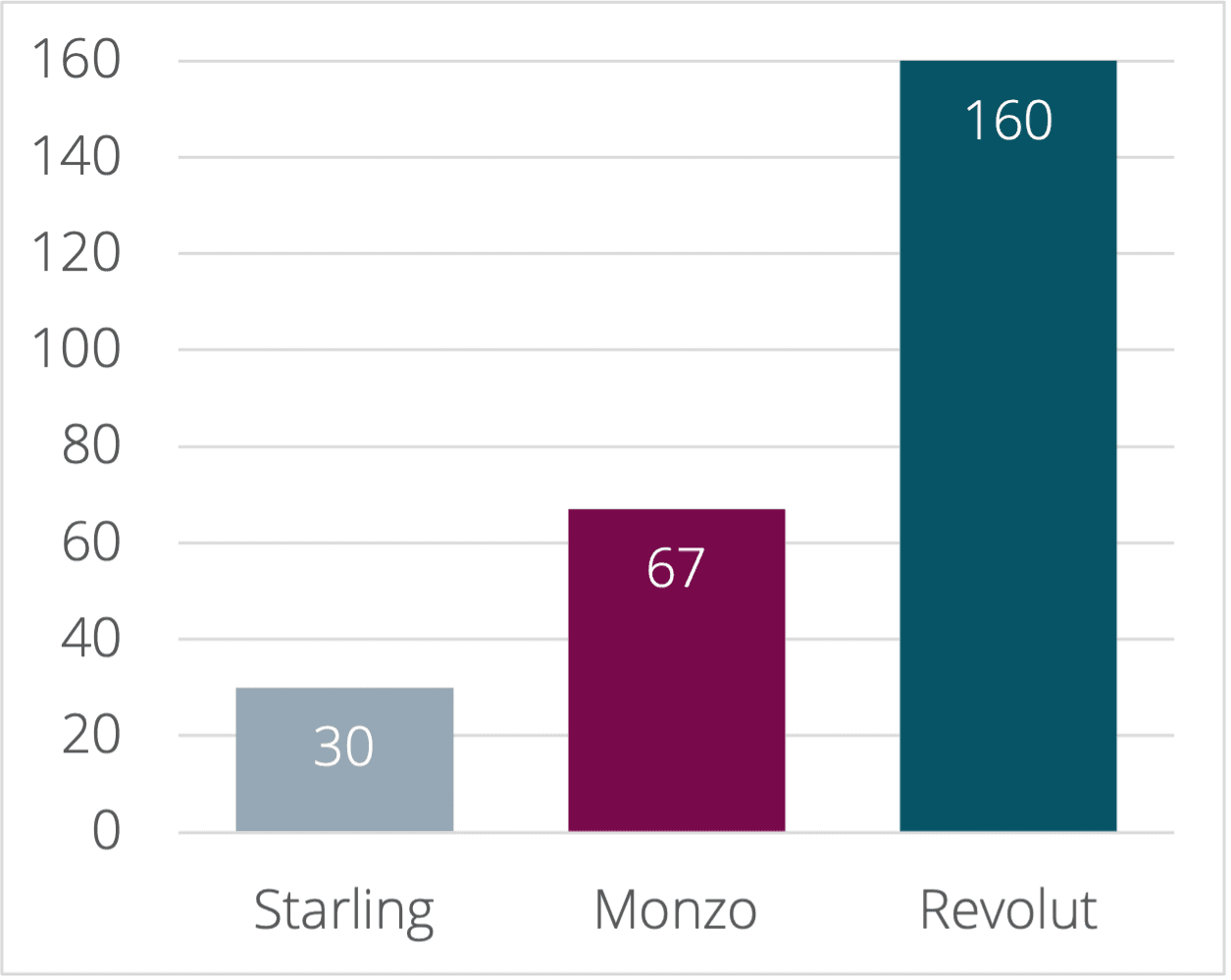

Revolut operates a “freemium” model, earning revenue through “interchange,” taking a small commission fee of 0.2% on each transaction – so as the user base grows, revenue follows. It also offers two paid-for premium tiers. Three years after launch, Forbes said Storonsky was “building the Amazon of banking” and described the app’s feature list as “simply encyclopedic,” with their product portfolio expanding well beyond the boundaries of the neo-banking sector. Revolut’s capacity to flex, expand and integrate partners and products into their portfolio ensures they can quickly solve customer problems that remain unaddressed by less agile businesses. Forbes points out that “Revolut’s strategy of building the best products in-house is certainly going against the grain, but it also seems to be working.” Starting in 2015 with fewer than 100,000 subscribers, Revolut has enjoyed explosive growth in recent years, increasing to 15 million today.

The numbers add up

Revolut’s funding history has been equally buoyant, having raised USD 900 million to date. Initially, the business was backed by Point Nine, Seedcamp, and Venrex and today boast investment from the veritable aristocracy of the investment world. This includes USD 250 million from DST Global in 2018 – tipping Revolut into unicorn status – and further investment in February 2020 led by TCV (known for their early investment in Facebook and Netflix). In February 2020, Revolut received USD 500 million in their Series D financing, with a valuation of USD 5.5 billion.

It is now believed that Revolut has engaged FT Partners (a US fintech-focused investment bank) to advise them on a new round of funding planned for later this year that will value the business at more than USD 10 billion. This would put Revolut among the most valuable technology companies ever created in Britain.

Revolut’s unit economics also looks robust, with revenues almost tripling in 2019 and user revenue increasing by 23% between 2019 and 2020. The business broke even in November 2020 despite the shaky pandemic conditions, and Storonsky confirmed the brand was 50% ahead in terms of revenue compared to pre-Covid levels. This is especially impressive given that cross-border payments declined globally during the pandemic.

Banking on expansion

Revolut currently has:

15 million personal customers

500,000 business customers

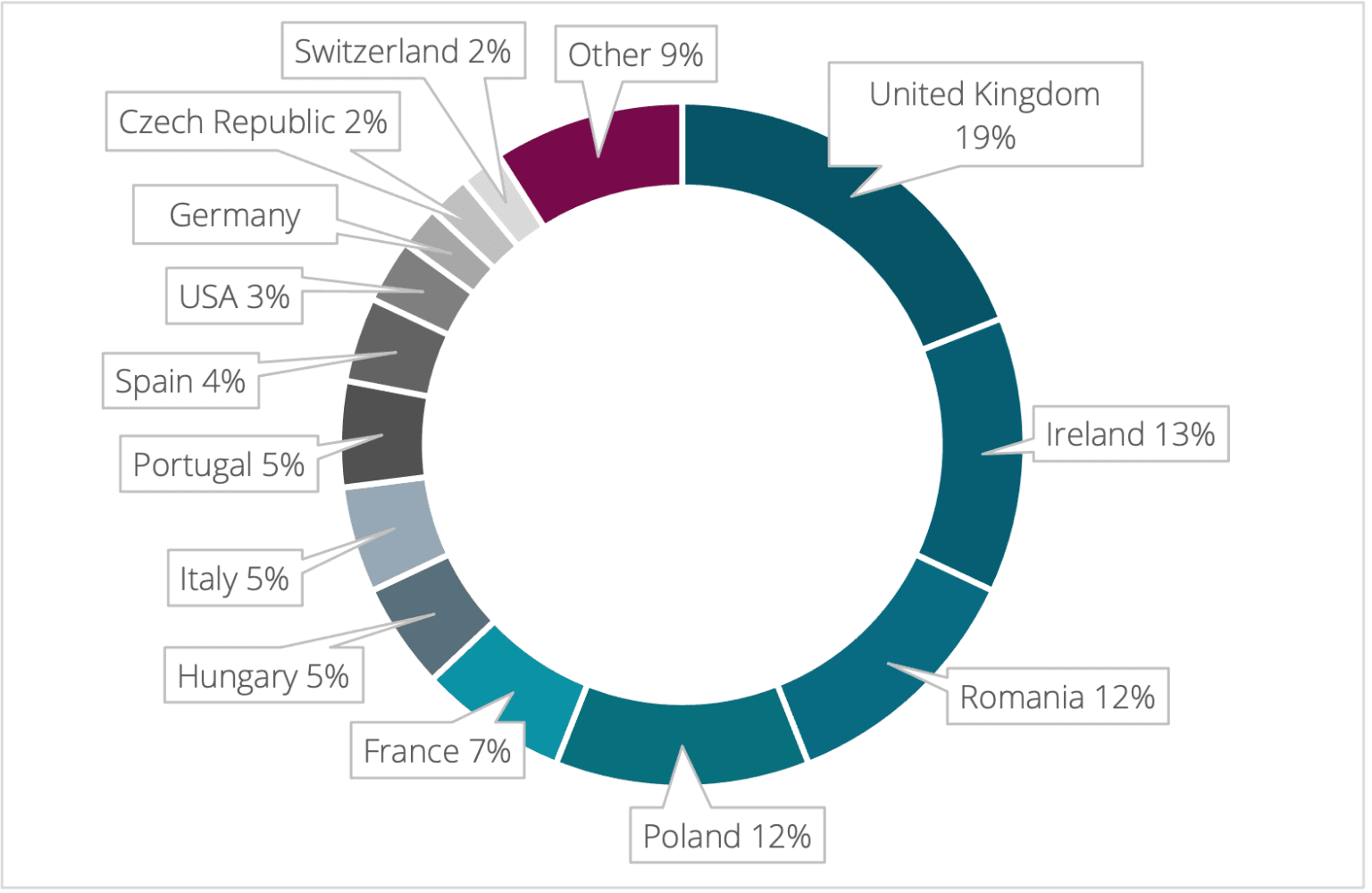

35+ countries supported

30+ in-app currencies

100 million transactions a month

2020 was a tumultuous year, and many European fintechs put their plans for expansion on hold. Not so for Revolut, who described 2021 as a “watershed year.”

After successful launches in Singapore and Australia in 2019, followed by Japan in 2020, Revolut is now turning its attention to the US and India. In March 2021, Revolut applied for a US banking license which would permit them to offer customers “all the essential financial products and services they can expect from their primary bank,” according to Storonsky. “Revolut has 200,000 clients today in the US, and our goal is to hit a million; that’s our first goal.” The business recently hired 300+ staff in Texas, making it their biggest US hub. This hub will focus primarily on Revolut’s business banking which the brand believes will make waves in the US market.

Revolut is also expanding into India, intending to have the app operational in 2022. Having recently recruited a 300-strong team, the Revolut India hub will also serve as an operations center for their global business.

The global neo-bank opportunity

Grand View Research confirms the global neo-banking market size was valued at nearly USD 35 billion in 2020 – ten times more than 2017. They forecast it will expand at a compound annual growth rate of 47.7% between 2021 and 2028, achieving a value of USD 722 billion+. Growth will be mainly powered by increasing demand for customer convenience. As neo-banks provide reduced transaction errors, real-time service offerings, improved customer experience, and low-cost, rapid delivery, their progress looks set to continue. Additional demand will also be driven by continued increases in smartphone penetration, where neo-bank demand is being propelled by the need for financial services on the go.

Europe and the US join the revolution

Europe dominated the neo-banking market in 2020, with 30%+ global revenue – driven by a large number of innovative technology companies and early adopters of new technologies. However, fintech adoption has also grown substantially in the US, with more than 24% of consumers interviewed by McKinsey utilizing a fintech banking platform and 6% of total consumers opening a banking fintech account during the pandemic. McKinsey’s research indicates that 40% of US consumers use a fintech platform for daily financial activities, and more than 90% are satisfied with their experience. These new fintechs now command consumer trust equivalent to traditional banks. In fact, Revolut’s Net Promotor Score is 77 – far outweighing HSBC (7) and JP Morgan (8). As fintechs outshine the traditional banks in multiple categories (convenience, ease of use, and experience), it seems the new players in the market are gaining ground.

A global super app

Revolut is aiming to become a single, unified global platform for financial services. Although not yet a fully-fledged bank, it does more than most neo-banks: handling money, transactions and currency exchanges, lending, and wealth management. It was one of the first neo-banks to merge traditional banking with cryptocurrency – enabling clients to buy and sell more than 25 coins. They currently employ more than 2,400 people globally, with their headcount nearly quadrupling over the last two years. Now chaired by veteran city big-hitters Martin Gilbert and Michael Sherwood, Revolut does appear to have the brains, brawn, and brand to go the distance.

Stableton can help you exploit this opportunity

At Stableton, our mission is to break down entry barriers to private markets and give you access to exclusive late-stage venture deals with investment amounts as low as CHF 10,000. We work with individual investors, institutions, and investment professionals to deliver these outstanding opportunities.

Introducing the Stableton Unicorn Index AMC

Learn how an allocation to the most exciting and rapidly growing privately held companies can help to boost your portfolio.

Contact Us

Call Us

Monday to Friday 8:00 a.m. to 6:00 p.m. (CET)

Direct Contact

Professional Investor Desk

Private Investor Desk

Poststrasse 24, 6300 Zug, Switzerland