Managed Futures

How investors can benefit from the disintermediation in banking

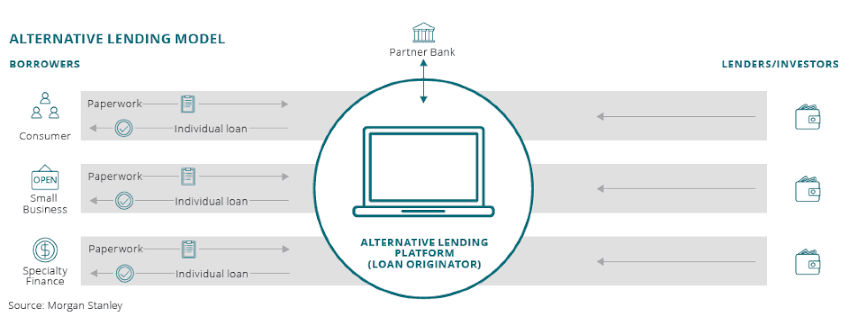

Before the global financial crisis, loan approvals relied heavily on personal relations and local expertise. The ensuing bank consolidation and centralization of loan approvals brought specific segments of the industry almost to a standstill. While the private equity industry jumped in to replace the larger-scale aspects of quasi-bank activities, the smaller, specialized end would only get serious attention with the recent advent of the fintech industry. Today, fixed-income investors can participate in the success of technology-driven lending platforms, who can approve financing often within minutes at rates in line with a fact-based risk model, and without the previously associated administrative burden. Alternative Lending is a fascinating segment that has risen from the ashes of the global financial crisis. Technology-driven startups and platforms are increasingly replacing banks when it comes to providing financing for small and medium-sized companies (SMEs) and private individuals alike. For investors, this novel approach can result in almost equity-like returns with the volatility of traditional bond investments. The distinctive characteristics of this segment also tend to make for little correlation to traditional stocks and bonds, therefore providing additional diversification benefits to the existing portfolio.

When obtaining traditional bank financing became tricky

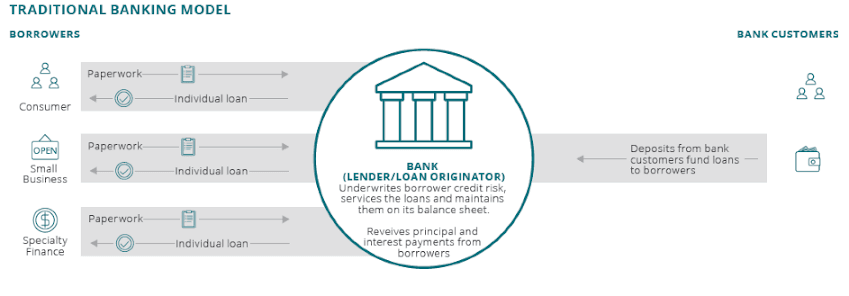

In the good old days before the global financial crisis, SMEs and private individuals would approach their trusted local bank for their financing needs. For a corporate or entrepreneur, those might have ranged from securing a business loan, invoice financing, asset-backed lending, trade or project finance, or agricultural loans. Individuals’ needs encompassed, for example, consumer loans, pawnbroking loans, car loans, or real estate financing.

Flawed credit approval processes as a contributor to the global financial crisis

The partner bank would work with the applicant to try and align the creditor’s quality with the bank’s risk appetite, which would subsequently result in the request being approved or denied. The credit approval process, in many cases, relied heavily on personal relations and local expertise. On the backdrop of a rallying economy in the mid-2000s, there is more than anecdotal evidence to suggest that individual and local considerations may not have positively contributed to the quality of loans issued. After all, the imploding real estate industry in the United States significantly contributed to pulling the rest of the world into a global financial crisis.

Lessons learned in the wake of the global financial crisis

With the consolidation of smaller banks and the ensuing centralization of loan approvals, both individuals and specialized businesses experienced increased difficulty in obtaining loans. Factors that contributed to this malaise were manifold. The newly-gained ‘objectivity’ by centralized loan officers at the same time meant that they lacked personal relationships with individuals and entrepreneurs, and only marginally understood the more specialized business models in their portfolios.

When approving SME loans became a career risk

Cost- and profit-margin pressure from the bank’s management resulted in selective approvals of loans that were profitable to the banks, and easy to assess. Also, loan officers took significant career risk by approving non-mainstream loans. Finally, the big bank’s internal processes led to long approval cycles, which thwarted time-critical loan applications. Innovation emerges from the ashes of the global financial crisis Post global financial crisis, this downward spiral intensified, essentially bringing certain types of loan approvals to a grinding halt. While segments of the private equity industry jumped in to replace the larger-scale aspects of quasi-bank activities, the smaller, specialized end would only get serious attention with the recent advent of the fintech industry.

With the help of newly emerging technology, new players in the market started to exploit the void created by banks. Increasingly, they started attacking the profitable segments banks had continued to hold onto as well.

Cloud computing, SaaS and artificial intelligence as drivers of alternative lending

Lending platforms and their Fintech operators have several advantages and trends going for them. For one, the wide-spread accessibility of distributed computing power and the availability of software-as-a-service (SaaS) gives them a cost and technology advantage over banks with their legacy IT systems.

More accurate decisions than any human could make

Secondly, the emergence of data science, artificial intelligence, and machine learning mean that they can build on open source solutions to crunch vast amounts of data, identify patterns and draw conclusions which loans to approve or reject with very high confidence ratios.

Financing can be secured within minutes at rates in line with a fact-based risk model

In real life, this means that today’s lending process has changed radically. A lender today can apply online and supply a selected array of data and information (as opposed to spending days filling out forms in the past). Based on this data, the platform’s system will analyze the received information against their dataset that contains highly accurate indicators of probable future loan delinquency or default. Consequently, the platform can then adjust the loan conditions dynamically. If those are acceptable to the lender, the loan will be approved often within minutes! The big banks are rushing to get back into this space. But their legacy systems, complex organizational setup and processes, and their high-cost structure will make this a formidable challenge.

Stableton’s approach to alternative lending

We believe that this attractive investment universe should be made available to qualified investors and their financial intermediaries through a single point of contact.

Stableton’s approach to the segment is to look beyond investment funds that indirectly allocate to securitized loan portfolios. Stableton prefers to partner directly with leading alternative lending platforms worldwide, with an initial focus on Switzerland, Germany, and selected countries in Europe that are operating at the forefront of the industry and applying stringent criteria.

This gives us unprecedented transparency into their loan books and the opportunity to diversify our approach across loan segments, credit quality, security interest, ticket size, duration, etc.

Our focus is on opportunities in the short-term end of the market

From a time horizon perspective, our current focus is on loan maturities up to one year as we feel this provides a less crowded market with a more predictable risk profile. Without being locked into multi-year loans, it allows us to make necessary adjustments should loan metrics worsen. This short time horizon also tends to result in an attractive yield-to-duration ratio. We are barely scratching the surface here. Please contact us below if you would like to discuss in more detail how you can efficiently access short-term alternative lending investments.

Introducing the Stableton Unicorn Index AMC

Learn how an allocation to the most exciting and rapidly growing privately held companies can help to boost your portfolio.

Contact Us

Call Us

Monday to Friday 8:00 a.m. to 6:00 p.m. (CET)

Direct Contact

Professional Investor Desk

Private Investor Desk

Poststrasse 24, 6300 Zug, Switzerland