Late-Stage Ventures & Neobanking

The old brick-and-mortar bank building is beginning to fade. In an age where everything seems to be accessible via an app, customers want convenience, and they want things to be different from the way they used to be. In terms of being able to take care of one’s finances, so-called neo-banking emerges as the answer. This subset of financial technology (fintech) is fundamentally changing how the world looks at banking, and with that, our relationship to money. In this article, we’ll take a look at what neo-banking is, its strengths and weaknesses, and what opportunities exist for late-stage venture investing in the neo-banking sector.

Neo-banking steps in where traditional banks drop the ball

Neo-banking refers to a new type of bank that has no brick-and-mortar branches. They are distinguished between credit-led and payment-led. Both types have different benefits and drawbacks. Credit-led neo-banks like Upgrade Inc. for example reach break-even faster and have a more robust foundation, but are harder to build due to the requirements. On the other hand, payment-led neo-banks like Revolut and N26 are scaling faster but reach break-even slower. Nevertheless, in both cases, everything is handled through mobile apps and websites. Money is transferred electronically end-to-end. Deposits are done via photographs. Client onboarding is easy, fast, and paperless. There are few, if any, fees. Many of these banks are tied to or developing other offerings, such as investing, credit cards, mortgage lending, and other innovative solutions we only begin to grasp.

There are over two billion people with internet connectivity, but no access to a bank

These startup upstarts are challenging the traditional banking business model and questioning what it traditionally meant to be a bank at all. One reason investors are pouring money into fintech, especially neo-banks, is because there are over two billion people on earth who have no banking relationship whatsoever. In other words, neo-banks are not only pulling existing customers from traditional banks but creating entirely new customer segments themselves. Many of those people who are currently unbanked have access to mobile networks. Yet, they were not attractive enough to traditional banks from a commercial perspective to justify building a remote bank branch. Neobanks have started filling that void right from the palm of a user’s hand.

Traditional banks will either try to compete or absorb their competition eventually

Many traditional banks are struggling to keep up. Even if they sink millions into strategic projects to build their versions of a neo-bank, the critical challenge is often breaking with old habits or challenging the status quo from within. Even seemingly simple things such as no overdraft fees and pay deposited two days early seem to amount to paradigm changes. Since destroying one’s business model from within is proving very hard to accomplish, the most likely course for established banks will likely be to eventually buy up a successful neo-bank and merge those services with their own. The most significant change happening now is that banking is becoming more consumer-friendly. Traditionally, banks charged fees on fees. There were all kinds of creative ways for banks to make money off their customers. With the advent of the neo-bank, the app generation has started turning its back on those practices, insisting that banks again demonstrate how much they value their customers’ business.

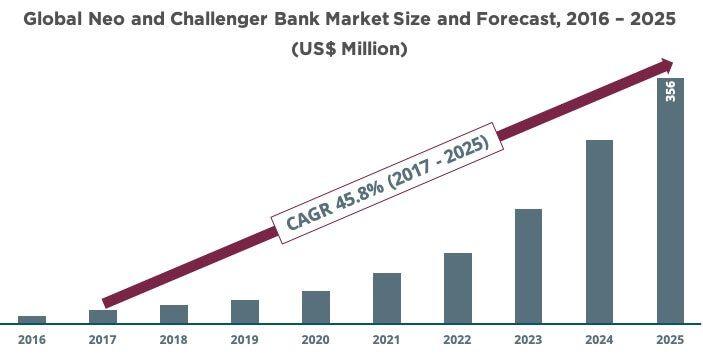

Neo-banking is growing at a staggering rate

With a compound annual growth rate (CAGR) of over 50% between 2017 and 2020, neo-banks and other banking challengers are tearing up the banking paradigm. We’ve all become accustomed to billions of hours of television on-demand and being able to order almost anything to be delivered to our doorstep in two days or less. Similarly, consumers are choosing the convenience of accessing the same services that their traditional banks offered, and much more, through an app. Without the red tape or wait times.

Neo-banks and other innovators are driving regulatory change

The new way of conducting banking has triggered a massive initiative to bring banking regulations that reflect the fact that the days are over when people would have a banking relationship through their local bank branch. Europe has led the world in clear and up-to-date regulations. They forged their oversight in conjunction with the neo-banks and other industry thought leaders. The Payment Service Directive Law, for instance, tore down one of the most important barriers to the rise of fintech: securing access to customer account data. In the US, the changes have been slower, with some claiming that they have been slow-stepped to some extent by the massive banks headquartered in the country. Simple things, like transferring funds from your neo-bank account to your investment account, are still blocked. The neo-banks have responded by simply creating investment branches that keep everything integrated. The laws regarding the actions of all non-banks will change as soon as consumers have moved in large enough numbers away from traditional banks.

Neo-banks take their time to turn profitable, but then make up for it handsomely

As with every other tech startup, neo-banks take time to turn a profit. But once they do, they are extremely profitable. One of the earliest disruptors, PayPal, is worth USD 50 billion. Other neo-banks are worth billions. Even the newer and small neo-banks are quickly worth hundreds of millions of dollars. Of course, valuation isn’t the same thing as profitability, but many of the more prominent neo-banks are beginning to show profitability.

The opportunity to invest in late-stage neo-banks

So-called late-stage investing in neo-banks, i.e., investing before they go public, can be an ideal investment, particularly in those that have a clear path to profitability and are being managed well. Of course, as with any other startup investment, there’s a risk that you can lose the money. Still, there are some clear frontrunners and runners-up in the neo-banking industry. If an investor wants to participate in the upside of the neo-banking revolution, getting in before the company goes public will usually yield much higher returns than waiting to buy their stock in the public market. When PayPal went public in 2002, it was valued at USD 13 a share with a valuation of USD 1 billion. Eighteen years later, that stock is traded at over USD 105, and the original investors are all now billionaires. The neo-banking industry is one of the most dynamic and profitable of the startup sectors. As noted earlier, the massive untapped market combined with a cultural shift among the largest living generation, the Millennials, make it a sector that’s likely to keep growing and becoming even more profitable. One might not even have to wait for, or worry about, the success of a potential IPO. As indicated previously, many neo-banks are likely to be scooped up by large financial institutions, which is another option for a successful exit. Particularly if the startup has assets or patented ideas that the big banks desperately want, the startup may never get to IPO. Its late-stage investors will get bought out at a handsome profit.

From growth to profitability

The title of the Business Insider 2019 neo-banking report says it all, “THE GLOBAL NEOBANKS REPORT: How 26 upstarts are winning customers and pivoting from hyper-growth to profitability in a $27 billion market.” There is a maturing happening in the neo-bank market for those startups that are in their second and third round of funding. They’re moving from a growth model to a profitability model. As the report notes, some of those features that are most attractive to consumers, such as no fees, are making profitability a little harder for these companies. Neo-banking is the wave of the future until it loses the “neo” moniker and is simply considered banking. The banking industry as a whole will have changed profoundly by that time.

There has never been a better time to invest in late-stage neo-banks

We know. “If I had a coin for every time, I heard that…!” In this case, it’s true. Here’s why: While neo-banking is, well, new, we have enough successful and money-making examples to be able to see the path to success. We’re not entirely blazing new trails. The acceptance of neo-banking is already massive, and it grows every day. Consumers are already on board. There’s still lots of room for growth and profits. We haven’t even gotten beyond infancy in this business. Innovation, built on the successes so far, will make neo-banking the future of how we handle our money. At Stableton, our mission is to help investors access the otherwise secluded late-stage venture investing market. With initial investments of as little at CHF 10’000, almost every investor can be a part of this future. We work with individual investors, institutions, and investment professionals to deliver these outstanding opportunities. Contact us today to learn more about late-stage venture investing.

Introducing the Stableton Unicorn Index AMC

Learn how an allocation to the most exciting and rapidly growing privately held companies can help to boost your portfolio.

Contact Us

Call Us

Monday to Friday 8:00 a.m. to 6:00 p.m. (CET)

Direct Contact

Professional Investor Desk

Private Investor Desk

Poststrasse 24, 6300 Zug, Switzerland