Volatility & Tail-Hedge

All-Weather Returns and Tail-Risk Protection

Except for the occasional correction, markets have been in a 10-year bull run

Market participants should start planning ahead for rougher times

One idea – a two-pronged approach that can turn volatility, and even a crash, into investment performance

Despite a few occasional hiccups, markets have been on a historic 10-year bull run. Globally, the macro picture is still looking decently good, as company earnings growth appears strong, and equity market valuations remain attractive, particularly relative to cash and fixed income.

Risk-taking is en vogue. Are we in for another round of the musical chairs game?

Those high market valuations, and an abundance of cheap money fuelled by low-interest rates, also led to investors becoming irrationally exuberant and increasingly careless. Even professional allocators have started to turn a blind eye towards the fact that, the longer this party lasts, the harsher the reality might sink in once the music stops playing. What happens to most portfolios once markets get choppy, or even crash? Is your portfolio all-weather proof?

Due to technological change, future market crashes could be more violent than expected

It does not take a long memory to imagine what happens in those instances. The last two decades have brought us the dot com bubble, the global financial crisis, the European debt crisis, and multiple flash crashes. Several of those crashes resulted in losses of more than 50% of capital. With automated trading systems becoming prevalent worldwide, the next crash could not only come without warning but surprise us with its violence.

Can returns be achieved in nervous markets? How can one protect capital should they suddenly correct?

Traditionally, installing any decent level of portfolio protection either meant buying put options or going into cash. The first method can be expensive and is somewhat frowned upon by professional investors. The latter, particularly if it lasted longer than a few days, would get any professional money manager into the delicate situation of not only having to explain why they charge fees for cash management but also the impact of negative interest rates on that cash! A two-pronged approach to dealing with difficult markets. The approach we have been focusing on trades quantitatively in the volatility asset class to harvest the volatility risk premium systematically. Also, it trades global equity index futures to benefit from big moves in equity markets. In a portfolio context, this should result in a negative correlation to equities and other asset classes.

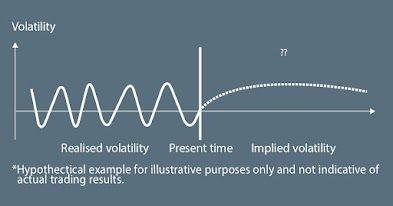

What is Volatility?

Volatility is a statistical measure of the variation of asset prices over a period of time. The market typically differentiates between two types of volatility: realized volatility and implied volatility. Realized volatility is a backward-looking measure of price variation calculated as the standard deviation of historical returns over a specified period. Implied volatility is a forward-looking measure of expected price variation that is implicit in market prices of options.

The Cboe Volatility Index® (VIX® Index) or sometimes referred to the “fear” index, for example, measures the implied volatility of the S&P 500 Index® (SPX) option prices. While the index itself is not directly investable there are liquid futures and options available. We are barely scratching the surface. Would you like to find out more about the details of this strategy, and how it could potentially fit in your existing portfolio?

Introducing the Stableton Unicorn Index AMC

Learn how an allocation to the most exciting and rapidly growing privately held companies can help to boost your portfolio.

Contact Us

Call Us

Monday to Friday 8:00 a.m. to 6:00 p.m. (CET)

Direct Contact

Professional Investor Desk

Private Investor Desk

Poststrasse 24, 6300 Zug, Switzerland