Returning to the Old-Fashioned Concept of Absolute Risk-Adjusted Returns

The concept of relative returns may be useful for benchmarking traditional mutual funds, but may not be nearly as good for our money.

Building wealth relies on compounding. Big, early losses defeat that purpose.

Not unlike in real life, return potential in investing must be evaluated against the unit of risk required to achieve it. Anything else means setting oneself up for disappointment.

Being the punching bag asset class when traditional markets rally

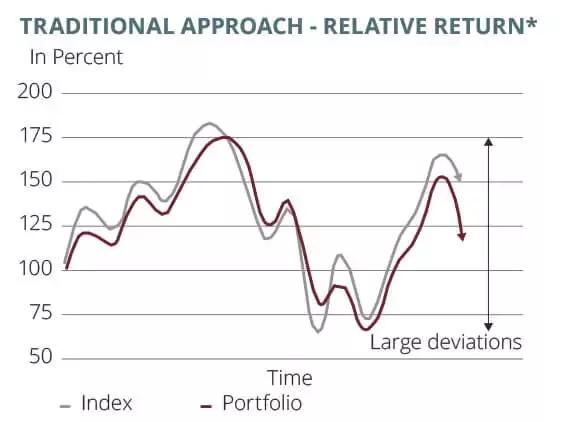

Anyone who has followed Alternative Investments over the years will have observed a curious pattern that spans economic cycles. As traditional markets rally, mainstream commentators tend to point out that stocks, bonds, gold, or crude oil, for example, are returning ‘more’ than the average Alternative Investment.

As markets turn south, the topic suddenly changes. Traditional stocks and bonds portfolios may have suffered a loss of 20 percent or more, yet many wealth management professionals tirelessly point out that equities fund x in their portfolio outperformed equity index y by three percentage points. Which still leaves an investor with a 17 percent capital loss on the investment! By their name, Alternative Investments are labeled as an alternative to traditional mutual fund types of investments, or mainstream asset classes such as listed equities or bonds.

Venture Capital, Private Equity, Hedge Funds, and Real Assets – segments as heterogeneous as they come

Alternative Investments are not a homogenous asset class like stocks and bonds. Venture Capital, Private Equity, Hedge Funds, and so-called Real Assets (such as Commodities, Real Estate, Agriculture, Timber, and even Art) are often referred to as Alternatives in literature. As if this were not confusing enough, the classification within each sector is also fluid. Some regard Venture Capital as part of Private Equity, since it is one of the early stages of a company life-cycle (others being Growth Capital, Buyouts, and Turnarounds/Distressed).

Classification might not just be difficult, but arbitrary, and most importantly, not relevant to an investor

There can also be some potential overlap between an active Buyout (Private Equity) fund and an activist special situations, a.k.a. Event-Driven Hedge Fund. There are more such grey areas, which only shows that the classification might not just be complicated, but arbitrary, and most importantly, not that relevant to an investor. What should be relevant to investors are other properties that separate Alternative Investments from traditional investments, i.e., mutual funds or exchange-traded funds.

Alternative Investments are about skill, regardless of where markets go

To avoid losses, and ensure predictable, sustainable performance, the best Alternative Investment managers are employing a specific mindset. As opposed to amateur investors, they don’t mistake their success for skill. They try to eliminate the concept of luck, be it bad or good luck, from their toolset. This approach includes understanding any factors that drive performance and isolating those they can influence from those they cannot (like market risk, i.e., markets behaving unexpectedly). Alternative Investment managers may want to reduce the impact of market risks, such as those of fluctuating stock markets and interest rates. This approach to risk reduction is in stark contrast to traditional asset managers who expose their capital (and with that, their investors) to these risks for their returns. After reducing their exposure to market risks, Alternative Investment managers pursue price inefficiencies and other dislocations to their superior understanding of every investment case.

Alternative Investments enjoy a wider playing field

A key characteristic of Alternative Investments is the freedom to look beyond traditional assets into areas such as alternative equity, market-neutral strategies, managed futures, volatility, tail-hedge, alternative lending, value-added real estate, and selected startups to a broader audience. This, for example, means looking beyond investing in publicly listed blue-chip companies that everyone is tracking, and where, due to the scrutiny of millions of eyes trained at them, opportunities are infinitesimally harder to uncover.

Alternative Investments need flexibility

To be able to apply their skill-set to an investment transaction and remove any unwanted (i.e., not manageable) risk, Alternative Investment managers often rely on a flexible toolset. While traditional asset managers can either hold an asset or not (stay in cash), Alternative Investment managers can also “short” an asset, i.e., sell a security to repurchase it at a lower price. They might not do this to purely speculate on lower prices as is often alleged in the media, but to neutralize, for example, market, sector, or interest-rate risk they already hold through their other assets. With those risks reduced or eliminated, Alternative Investment managers may also employ some leverage, resulting in long and short assets temporarily exceeding overall fund assets. However, this type of leverage-taking can actually lower the overall risk compared to traditional asset managers. While we will deal with the risk profile of Alternative Investments in a subsequent post, let us remark that most of us have more leverage in our home mortgage than the average hedge fund employs in their daily work. In terms of the toolset, some have used a golf analogy to explain Alternatives vs. traditional investments. While the former can play with a full set, the latter is restricted to only a few clubs. We would argue that having more tools at one’s disposal increases the chances of being successful, provided one is versed in using them.

With the help of newly emerging technology, new players in the market started to exploit the void created by banks. Increasingly, they started attacking the profitable segments banks had continued to hold onto as well.

Stableton’s approach to Alternative Investments

We agree with US comedian Will Rogers who famously stated that he was more concerned about the return of his money than with the return on his money. The proper implementation of an absolute return strategy does not only entail a significantly lower risk of a significant capital loss – as there is no rigid link to a benchmark – but usually also considerably more calculable investment results.

Stableton’s approach to alternative lending

We agree with US comedian Will Rogers who famously stated that he was more concerned about the return of his money than with the return on his money. The proper implementation of an absolute return strategy does not only entail a significantly lower risk of a significant capital loss – as there is no rigid link to a benchmark – but usually also considerably more calculable investment results.

Introducing the Stableton Unicorn Index AMC

Learn how an allocation to the most exciting and rapidly growing privately held companies can help to boost your portfolio.

Contact Us

Call Us

Monday to Friday 8:00 a.m. to 6:00 p.m. (CET)

Direct Contact

Professional Investor Desk

Private Investor Desk

Poststrasse 24, 6300 Zug, Switzerland