BNPL 2.0 – The Business Model Poised to Replace the Credit Card

2020 was a turbulent year in every way. The global payment sector certainly felt the effects, experiencing its first revenue contraction for 11 years due to the pandemic-prompted economic slowdown. As lockdowns hit country after country, people were confined to their homes, and spending was diverted online. As a result, businesses rushed to digitalize, and innovative online payment models emerged or gained new momentum. Part of this shift is the new buy-now-pay-later (BNPL) movement, ostensibly a point-of-purchase financing product evolving into fully integrated shopping experiences. The Washington Post suggests these services have grown as much as 200% during the pandemic.[1] As BNPL and its myriad of opportunities develop, investors would be wise to watch significant players within the sector. Since some of those key players are in their late venture or pre-IPO stage, being able to invest into one of them before they list publicly can deliver exciting results. It is a chance to get a slice of proven innovation before the scramble of an oversubscribed IPO.

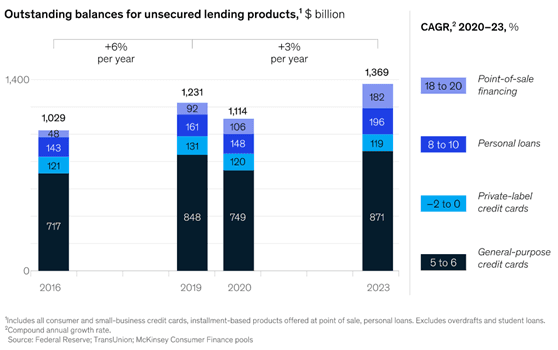

BNPL reinvented for the digital age Deferred payments have long existed in the financial landscape. Historically, they helped make larger purchases affordable by financing them over a more extended period through interest-bearing loans. The new BNPL models are innovative and answer a consumer need spurred by both the global financial crisis of 2008 and the global pandemic. Economic instability and job insecurity left consumers wary of credit, and credit cards in particular. Klarna’s chief marketing officer describes this in colorful terms: “What we’re seeing now is a whole generation abandoning credit cards. Roughly 70% of American millennials don’t have a credit card because they fear them more than they dread death, according to some reports.” Statista explains that credit card debt is often stated as a reason for being unable to buy a house in the US.[2] Indeed, the younger generation distrusts credit card companies, perceiving them to have exploited their position by charging high rates and lending irresponsibly. The open-ended nature of credit-card debt is also a concern to these consumers, who are anxious about even being accepted for a credit card. The BNPL model of having a separate credit agreement for each purchase addresses these concerns. In addition, BNPL credit checks are often a less stringent “soft search” invisible to other lenders on the consumer’s credit file. Of course, this approach puts more of the onus on the consumer themselves to determine whether they can afford the repayments, instead of the lender making assumptions based on their existing borrowing. But the more transparent nature of the BNPL business model appeals to credit-skeptical consumers. Max Levchin, the co-founder of PayPal and the BNPL brand Affirm, says his inspiration was to “build an alternative to credit cards that is built around a sense of transparency and clarity, you know, both what can you spend, exactly what it will cost, exactly what is and isn’t good for you financially”. Merchants pay to eliminate credit and fraud risk while gaining data-driven consumer insights BNPL’s most lucrative revenue stream is from the merchants who use their services. The BNPL brand usually charges a fixed transaction fee and a variable percentage of the customer’s transaction. In return, the merchant eliminates exposure to both credit and fraud risk and gains access to valuable, data-driven consumer insight, referrals, and the seamless integration of the payment solution into the retailer’s website. Shoppers using BNPL spend more and buy more frequently Previously, retailers had been nervous about BNPL eating into their own private-label credit card business, but rapid adoption and repeat business have seen merchants sign up in droves. BNPL brands also add trusted credentials and credibility to a broad spectrum of retailers and merchants. Ted Rossman, an analyst at creditcards.com, found that shoppers who use BNPL options also tend to spend more and buy more frequently than those who do not, and merchants’ attribution figures demonstrate this.[3] This is a symbiotic relationship with merchants delivering impressive revenue; Forbes states that, in the quarter ending September 2020, a third of Affirm’s revenue came from a single client: Peloton.[4] Players to watch in the BNPL sector Klarna Tipped to list publicly in 2023, the Swedish fintech Klarna pioneered BNPL with an app that allowed consumers to split the cost of purchase into more manageable, interest-free chunks. Their innovative app is a shopping destination that delivers targeted, bespoke content and personalized experiences that consumers respond to very positively. As a result, Klarna enjoys an NPS score[5] of between 65 and 72, compared to the traditional banking average of 34. With 250,000 merchants and 90 million consumer users, Klarna achieved tridecacorn status in March 2021 and is currently Europe’s highest-valued privately held fintech. Affirm Publicly traded Affirm was founded in California in 2012. Max Levchin, Affirm’s co-founder, had previously launched PayPal, the gaming company Slide, and the fertility-tracking app Glow. The Affirm product is already used by nearly 9 million consumers and featured at more than 100,000 retailer checkouts.[6] Even if it is not offered, it is still possible to pay in installments using an Affirm virtual credit card or the Affirm app. Amazon has a partnership with Affirm, which is widely believed to be Amazon’s way of determining whether they will acquire Affirm or build their own BNPL product. Afterpay Australian BNPL Afterpay (known as Clearpay in the UK, France, Italy and Spain) was recently acquired by the payment company Square for $29 billion. With 11 million active users and nearly 64,000 merchants,[7] Afterpay operates across ANZ, the US and Europe. The acquisition brings Afterpay’s network of merchants into Square’s network for conversion. Square plans to offer BNPL functionality to customers of their existing Cash App facility (their fast money transfer service). The Afterpay business uses smart credit limits and an instant approval decision for each purchase to ensure customers can afford their payments. Sezzle Minneapolis-based Sezzle is a publicly-traded, B Corp certified BNPL firm operating in the US. It currently has 3.2 million active customers and around 45,000 active merchants on its platform. Sezzle’s value proposition is the ability for customers to schedule their repayments more flexibly to suit their circumstances. Australian BNPL provider Zip is currently in discussion with Sezzle regarding a possible acquisition. This follows its acquisition of Quadpay and would bolster its offering further. PayPal Pay in 4 One of the online payment pioneers, PayPal is a trusted brand name on many merchant websites. More than 80% of the 100 leading US retailers currently use the PayPal platform. Its newly introduced “micro-loan” service, Pay in 4, was launched in the US last year. It joins its growing portfolio of payment options, including PayPal Credit, Easy Payments and Pay After Delivery. Doug Bland, SVP of Global Credit at PayPal, confirms: “With Pay in 4, we’re building on our history as the originator in the buy now, pay later space, coupled with PayPal’s trust and ubiquity, to enable a responsible and flexible way for consumers to shop while providing merchants with a tool that helps drive sales, loyalty and customer choice.” The blistering pace of change looks set to continue The value of the BNPL landscape is thriving. The Research and Markets Q4 2021 BNPL Survey predicts that the Global BNPL payment industry is expected to grow by more than 60% annually, reaching USD410 billion in 2022.[8] BNPL payment adoption is expected to grow strongly, achieving a CAGR of 32.7% during 2022-2028. Changing consumer behavior, the pandemic, and ultra-low interest rates have all generated momentum within the sector. Against this backdrop, fintechs look likely to capture much of this value, being created as the banks have been slow to respond (Goldman Sachs and Monzo have only recently entered the sector). In addition, BNPL providers will continue to collect increasingly rich data around consumer preference and behavior, becoming more valuable partners to merchants than traditional banks or credit companies. As a result, smart investors keep a watchful eye on the key players in this sector. Contact Stableton or sign up to explore our investment opportunities In the past, accessing the opportunities such those offered by the BNPL segment meant seeking early access through venture capital funds (which, once well-established, might not even be interested in your commitment). In addition, it involved high investment minimums, cumbersome paperwork, scarce information (often not even knowing what you will be investing in), and long holding periods. Today, there is an alternative. Accessing promising businesses via late-stage investment and pre-IPO investments is increasingly popular. For one, investors know the name of the company they are investing in. Secondly, as in the case of certain key players in the BNPL segment, the product-market fit has already been established, and the path to profitability is clear. To hop on an investment at this stage means a lot of upside potential, while the risk level stays relatively moderate. Stableton is Switzerland’s leading provider for access to late-stage venture capital & pre-IPO Investments to smaller qualified investors. Our mission is to help investors get access to the otherwise secluded private investment market. With a minimum of CHF 10’000, this type of investing should be considered as part of a portfolio. This article only scratches the surface of the opportunities late-stage VC and pre-IPO investing present. Contact your Stableton representative now to learn more and find out about opportunities that exist right now.

Introducing the Stableton Unicorn Index AMC

Learn how an allocation to the most exciting and rapidly growing privately held companies can help to boost your portfolio.

Contact Us

Call Us

Monday to Friday 8:00 a.m. to 6:00 p.m. (CET)

Direct Contact

Professional Investor Desk

Private Investor Desk

Poststrasse 24, 6300 Zug, Switzerland